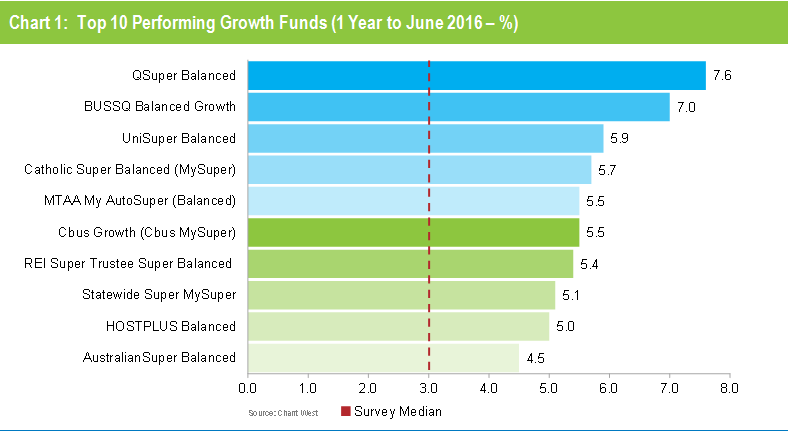

Australia's major super funds weathered a late Brexit scare to post their seventh consecutive positive financial year return. The median growth fund returned 3% in 2015/16, while the top-performing fund – QSuper – delivered 7.6%. All funds in the Growth category posted positive returns for the year. Growth funds are those that have 61 to 80% of their investments in growth assets and are the ones in which the majority of Australians are invested.

While the 2015/16 return is significantly lower than those of the previous three years, Chant encourages members to think long term. "Most people working today will eventually convert their super into income streams to live on, so that money will stay in the super system long after they retire. It really is a lifetime investment, and there will be good times and bad times along the way. We're currently in a period of lower returns and higher volatility, and that may continue for some time. What's important is to know what your fund’s risk and return objectives are and whether they're achieving them.

"Funds themselves think long term, and some of them are now reflecting that by setting their objectives over periods as long as 10 years. Typically, though, the return objective is still to beat inflation by 3% to 4% per annum over rolling five year periods. We now have data going back 24 years to July 1992, which is when compulsory super was introduced. When we look back over that very long period, we find that the annualised return is 8.1% and the annual CPI increase is 2.5%, so the real return above inflation has averaged 5.6% per annum. So over the longest period we can measure funds have well and truly met their return objective.

"That's borne out visually in Chart 2, which compares the growth category median with the average return objective for funds in that category (CPI plus 3.5% per annum after investment fees and tax over rolling five year periods).

Note: The CPI figure for the June quarter is an estimate.

"Until the GFC hit, the median fund outperformed the target most of the time. The GFC brought that to an abrupt halt, and the median fund dipped below the target line for several years. Now, with the GFC period having worked its way out of the calculation, the five year return has again been tracking above the target line for nearly three years.

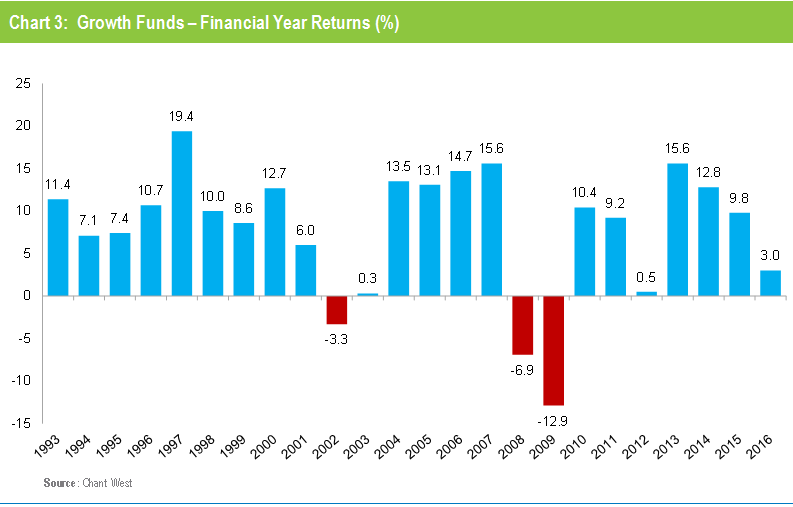

"In addition to their return objectives, most funds also set themselves a risk objective. Typically, for a growth fund, this is to post a negative return no more often than once in every five years on average. Chart 3 plots the year by year performance of the median growth fund over the full 24 financial years since the introduction of compulsory super. In that time, there have been three years when returns were negative. That averages out to one year in eight, so the risk objective has also been met.

Note: Performance is shown net of investment fees and tax. It does not include administration fees or adviser commissions.

"So the message is that, while the 2015/16 return may not have set the world on fire, over the longest period we can measure Australia's major super funds have done what they set out to do in terms of risk and return."

The investments that drove the performance

While there are differences between funds' investment strategies, even within the same risk category, most of their performance is driven by what happens in the major investment markets. For growth funds, that is primarily the Australian and international share markets, because those are the sectors where they allocate most of their money.

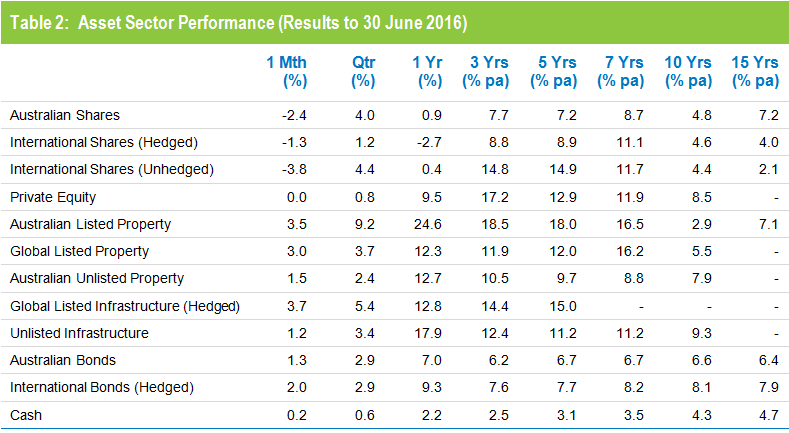

Table 2 shows the performance of all the main asset sectors over different time periods. We have used market indices for all sectors other than private equity and unlisted infrastructure. For those sectors, for which no indices exist, we have used the returns of a major fund in our survey that are representative of those markets.

Source: Chant West

The key points to note for the 2015/16 financial year are:

- Australian shares only just made it into positive territory with a return of 0.9%.

- Hedged international shares retreated 2.7%. However, the depreciation of the Australian dollar (down from US$0.77 to US$0.74) meant that this translated into a small gain of 0.4% in unhedged terms.

- Australian listed property was the best performing asset sector with a very strong return of 24.6%. Unlisted Australian and global listed property also produced healthy returns of 12.7% and 12.3%, respectively.

- Unlisted infrastructure and global listed infrastructure also generated strong returns 17.9% and 12.8%, respectively. Private equity returned a solid 9.5%.

- The main defensive asset sectors all delivered positive returns. Australian and international bonds gained 7.0% and 9.3%, respectively, easily exceeding the cash return of 2.2%.

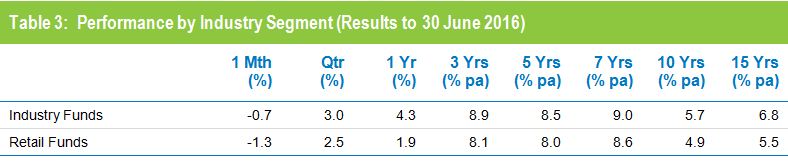

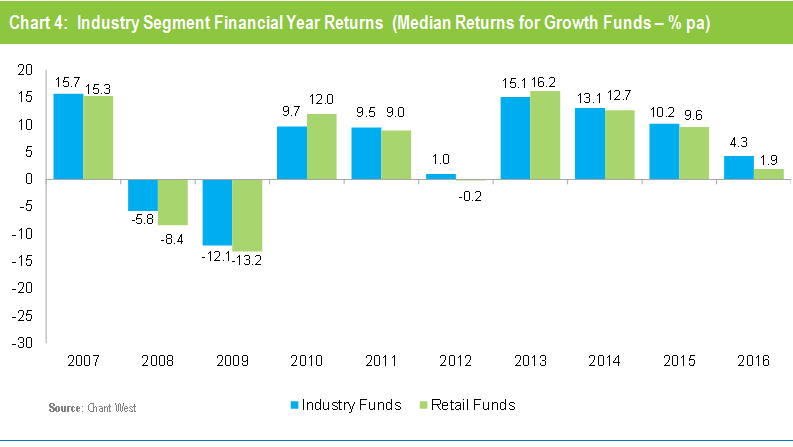

Industry funds ahead of retail funds over the year and longer term

Industry funds outperformed retail funds over the year, returning 4.3% versus 1.9%. Industry funds also hold the advantage over the longer term, having returned 6.8% per annum against 5.5% for retail funds over the 15 years to June 2016, as shown in Table 3.

Source: Chant West

Note: Performance is shown net of investment fees and tax. It is before administration fees and adviser commissions.

Chart 4 compares the performance of the two segments year by year over the past ten years.

Chant says: "Over the longer term, industry funds have outperformed retail funds largely because, as a group, they tended to have lower allocations to listed shares during periods when shares underperformed. While that historical difference in allocation no longer applies, they have also had higher allocations to unlisted assets such as private equity, unlisted property and unlisted infrastructure which have performed well for them. That difference still applies, with industry funds currently investing 20% in these sectors against 5% for retail funds, and that goes some way to explaining their outperformance over 2015/16.

"Over the longer term, the asset allocation policies of industry funds have served them very well. Those allocations to unlisted assets do mean slightly higher investment costs, but those extra costs have been more than justified by the better performance and lower volatility.

"Industry funds have also been more prepared to shift away from their longer-term target asset allocations to take advantage of mispricing or to preserve capital. Overall, those medium-term shifts have had a positive effect on their performance."

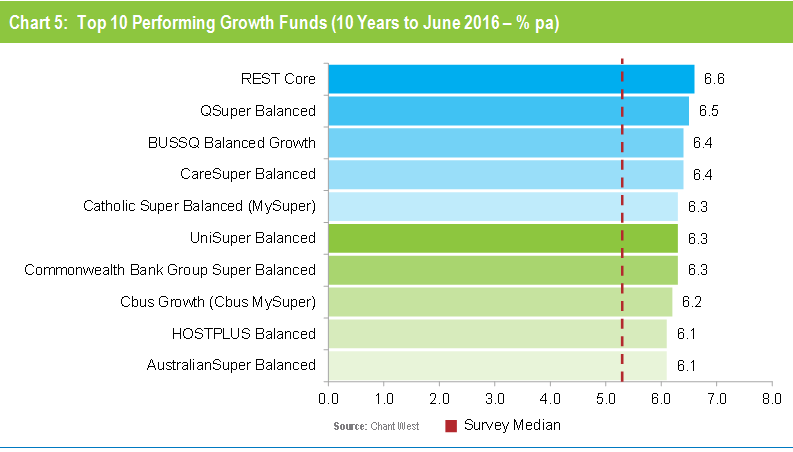

Chart 5 shows the top 10 performing funds over ten years. As has been the case for many years, the list is dominated by industry funds which account for eight of the ten places. The other two places are occupied by QSuper, which is a non-profit fund primarily for Queensland public servants, and the stand-alone fund for employees of Commonwealth Bank.

Notes:

1. The top 10 is limited to growth options with assets of $1 billion or more.

2. Performance is shown net of investment fees and tax. It is before administration fees and adviser commissions.